Every now and then a new word or phrase is introduced into the conversation. On November 8, 2016, it was demonetisation. It was portrayed as the white knight on a steed who will slay the demons of black money, corruption and fake currency.

Six weeks later, the demon of black money continues to flourish. The tax evaders do not seem fazed by demonetisation, they are accumulating black money in the new currency! They have traded their old notes for new notes. According to the Income-Tax Department, since demonetisation, it has seized Rs 500 crore in cash of which Rs 92 crore was in new Rs 2,000 notes.

The other demon of corruption is still alive. Officials of the Kandla Port Trust, engineers of the Military Engineering Service, RBI officials, bank and post office officials, and many others have been caught red-handed taking bribes in the new Rs 2,000 notes.

The third demon is fake currency. Just wait for a few months and it will be proved that printing technology is indifferent between the crooks and the RBI. The counterfeiters will soon acquire the

technology and challenge the Reserve Bank of India to stay one step ahead.

Panic attack

The unravelling of demonetisation caused panic in the government. The first sign was when the government and RBI began to renege on their promises and changed the rules repeatedly (at last count 62 times!).

The value of notes that could be exchanged was raised, then lowered, and it was stopped altogether on November 24. Indelible ink was used to mark the finger, then discarded. The withdrawal limit of Rs 24,000 per week remained only on paper and most people got paltry sums.

Permissible use of old notes was abruptly stopped on December 15. The ultimate panic reaction was when the RBI ordered that one could deposit old notes only once and up to Rs 5,000 (without being asked questions) after December 19 and before December 30, putting paid to the promises of the Prime Minister and the Finance Minister. The Finance Minister offered lame clarifications. Two days later, the RBI was shamed into reversing its directive.

The Prime Minister realised soon that he had been convinced or conned to buy a lemon. He had no choice but to change the narrative. He propounded the idea of a ‘cashless economy’. In his speech on November 8, the Prime Minister did not once use the word ‘cashless’. It was all about ‘black money’ (18 times) and fake currency (5 times). By November 27, the Prime Minister shifted gears and in two speeches that day he mentioned ‘cashless’ 24 times and ‘black money’ only 9 times!

‘Cashless’ economy is not an innocent or harmless goal. It conveys a compete lack of empathy for the poor and those who have minimal or no access to the digital world.

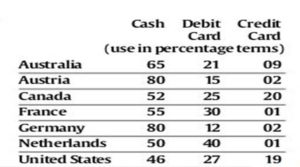

Not a cashless world

No economy has become ‘cashless’, not even the most developed economies (see table):

(Source: Bloomberg)

(Source: Bloomberg)

The value of dollars and euros in circulation has doubled since 2005 to $1.48 trillion and € 1.1 trillion respectively. The US and Europe are using more cash, not less cash!

World over, the necessary and desirable rule is that people must have cash in their hands and be able to carry out routine transactions using cash. It is perfectly legitimate for a government to make a law that high-value transactions shall be by cheque or any mode of digital payment — examples are real-estate transactions, high-value jewellery, large contractual payments, debt repayments, payment of certain taxes etc.

On the other hand, to insist that a farmer shall pay hired labour in digital mode or a homemaker shall buy vegetables by swiping a card is an unwarranted intrusion and puts an oppressive burden upon the payer and the payee. Remember, there is a cost to digital payment that will be borne by the consumer. Subject to a reasonable law concerning high-value transactions, we must have the freedom to choose the mode of payment. That is our right and no government should be allowed to interfere with that right.

A distracting mirage

Consumers may be divided into three categories based upon the degree of access to the digital world: real access, minimal access and no access. 71 crore debit cards have been issued so far; in August 2016, these cards were used to withdraw from ATMs Rs 2,19,657 crore but were used to make payments of only Rs 18,370 crore. To put a card or a smartphone in everyone’s hand, to provide real access to everyone, and to make everyone adopt the digital mode will require advocacy, education and persuasion, not coercion — and without restricting the person’s fundamental right to use cash.

There is also another important issue — privacy. Why should a young adult be forced to disclose that she bought lingerie or shoes or he bought liquor or tobacco? Why should a couple be forced to leave a trail of a private holiday? Why should an elderly person leave a record that he bought adult diapers or medicines for his ailments? Why should the government or its numerous agencies have access to our lives through access to Big Data? I think these questions need to be debated before the country is pushed into embracing the digital mode for all monetary transactions.

Cashless India is an illusion. It is a distracting mirage. It may not even be a desirable goal.

Website: pchidambaram.in @Pchidambaram_IN

{kind=link}